It is not everyday that there is a long New Yorker article sitting squarely in my field — innovation strategy. But this week we have one by Jill Lepore who conducts a systematic ‘take down’ of Clay Christensen. For those of you who have read Christensen’s work and found his cases convincing, Lepore pulls them to bits in ways that are not really new but at least tell you that those cases were hardly a foundation for a new theory of innovation that is sold as applying to everything.

It is not everyday that there is a long New Yorker article sitting squarely in my field — innovation strategy. But this week we have one by Jill Lepore who conducts a systematic ‘take down’ of Clay Christensen. For those of you who have read Christensen’s work and found his cases convincing, Lepore pulls them to bits in ways that are not really new but at least tell you that those cases were hardly a foundation for a new theory of innovation that is sold as applying to everything.

There are so many ways in which Christensen is an easy target. One is that the “theory of disruptive innovation” has been remarkably successful. The word “disruption” has gone from bad to good, from poor TV reception to happening everywhere. All of the noted tech leaders of the past two decades have been influenced by Christensen, including Steve Jobs who took the theory to heart in producing the iPhone and iPad even as Christensen, himself, decried the iPhone as doomed to fail. The word “disruption” is used too often which means that Christensen is an easy mark precisely because that mark has become so wide.

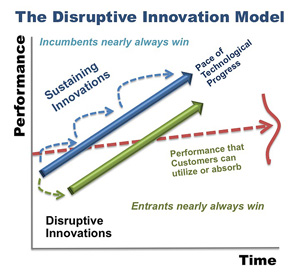

But for every theory that reaches too far, there is a nugget of truth lurking at the centre. For Christensen, it was always clearer when we broke it down to its constituent parts as an economic theorist might (by the way, Christensen doesn’t like us economists but that is another matter). At the heart of the theory is a type of technology — a disruptive technology. In my mind, this is a technology that satisfies two criteria. First, it initially performs worse than existing technologies on precisely the dimensions that set the leading, for want of a better word, ‘metrics’ of the industry. So for disk drives, it might be capacity or performance even as new entrants promoted lower energy drives that were useful for laptops.

But that isn’t enough. You can’t actually ‘disrupt’ an industry with a technology that most consumers don’t like. There are many of those. To distinguish a disruptive technology from a mere bad idea or dead-end, you need a second criteria — the technology has a fast path of improvement on precisely those metrics the industry currently values. So your low powered drives get better performance and capacity. It is only then that the incumbents say ‘uh oh’ and are facing disruption that may be too late to deal with.

Herein lies the contradiction that Christensen has always faced. It is easy to tell if a technology is ‘potentially disruptive’ as it only has to satisfy criteria 1 — that it performs well on one thing but not on the ‘standard’ stuff. However, that is all you have to go on to make a prediction. Because the second criteria will only be determined in the future. And what is more, there has to be uncertainty over that prediction.

To see this, suppose that it was obvious that criteria 2 was satisfied. Then it will be obvious to all — entrants and incumbents — what the future might look like. This is precisely what happened for web browsers when Microsoft ‘wised up’ and saw the trajectory. In that situation, a disruptive technology does not end up disrupting the establishment at all. They have seemingly an equal shot of coming out on top: indeed, a better shot when you consider they already have the customers.

What is required for the theory to be complete is that it is not known whether criteria 2 is satisfied or not. That is what creates the ‘dilemma.’ For an incumbent, it is costly to bet on a new, unproven technology when things are going fine with the old one. And as Lepore points out: there are plenty of situations where incumbents have gone with the new too soon only to have huge losses as a result. Christensen takes on this nicely: basically saying that incumbents are essentially doing the right thing even though they might be doomed. It is the twist that offends no-one while generating fear and debate.

If it had all stopped there, this would have been respectable. But Christensen did not. He saw his theory as predictive even though its own internal logic says prediction is impossible. That’s why he missed the mark on the iPhone. That is why his case studies can be right unless you wait a little longer in which case they are no longer predictive. The Innovator’s Dilemma is like Heisenberg’s Uncertainty Principle. You can’t get around it and Christensen’s failing is that he has sold it as something you can get around.

Take his prescription that established firms ‘disrupt themselves.’ This is crazy talk to an economist (which is one reason he doesn’t like us). Suppose you take resources and invest in your own disruptor. If disruption occurs, you still lose the entire value of your existing business. All that has happened is that you have kept your name alive. The retort may be that something can be preserved but remember, Christensen is essentially saying firms need to act as if nothing can be preserved. I don’t mind the idea that established firms should not be complacent but hastening their demise on speculation seems weird when there is no upside.

Instead, the focus on the doomed incumbent leads Christensen away from the obvious alternative. The incumbent should ‘wait and see.’ They will see all manner of potentially disruptive technologies being deployed and instead of removing them from their radar as irrelevant, they should continue to monitor them to see what happens. Because, when the one in ten or a hundred or whatever turns out to be successful, they can then move to acquire them and realise a more ‘orderly transition’ to the new technology. Indeed, as I read Lepore, I got the sense that even with Christensen’s iconic examples, the end result was incumbent preservation through acquisition. And this is not just theorising. My own recent paper with Matt Marx and David Hsu demonstrates just that: disruptive technologies (identified after the fact) are associated with start-ups competing and then being acquired as much as they are associated with those start-ups growing as independent firms.

And there is one final wrinkle in all of this. What of the prescription that entrepreneurs find industries to disrupt? This is not a bad notion as this can focus you on consumers who are under-served by current incumbents. But I am always reminded of the final (after the credits) scene in Finding Nemo where the fish from the dentist’s tank finally escape and end up in Sydney Harbour in plastic bags saying “now what?” If you disrupt an incumbent, surely you have to ask “now what?” The future is one of relentless competition and margins driven down to nothing. That is hardly the vision of a great return on venture capital investment. Take the classic relentless disruptor of Amazon as a case in point. Disruption is everywhere they touch but in their bottom line.

Lepore only deals with the easy marks in her take down of Christensen and one suspects Christensen and his supporters can easily fend those off. It is the fundamental contradiction in taking a positive theory towards prediction that is where this entire ‘disruption industry’ falls down. I’d like to see journalists engaging more on that level so that we can be done with those bridges too far for good.

“Criterion” not “criteria” for singular.

Good Article Joshua – you may not remember me, but I was a student in your macro-economics class in AGSM in 1996. I just released my second book titled Outsourcing 3.0 – check it out.

As far as the model above is concerned – I agree with you. I would like to add that I find the model of disruptive seriously flawed because of so many flawed assumptions embedded into it. The key question is – Why can the customer not absorb or utilise new technology? Why would you call something innovation, if it cannot be absorbed or utilised by the customer? Steve Jobs had no such problems with iPhone – people learnt intuitively how to use it. Is not the usability one criterion for success of innovation? The term ‘disruptive’ is also a misnomer in this context.

“Take his prescription that established firms ‘disrupt themselves.’ This is crazy talk to an economist (which is one reason he doesn’t like us). Suppose you take resources and invest in your own disruptor. If disruption occurs, you still lose the entire value of your existing business. All that has happened is that you have kept your name alive. The retort may be that something can be preserved but remember, Christensen is essentially saying firms need to act as if nothing can be preserved. I don’t mind the idea that established firms should not be complacent but hastening their demise on speculation seems weird when there is no upside.”

I think a basic idea here is that this stuff, like so much in life, is quite case-by-case. The particulars really matter, like with the iPhone, where the particulars were very strong, but unlike the Lisa, where they were not, yet. And you consider the likelihood of the threat, how soon, time-value-of-money, and so on. This is all if your goal is just to maximize corporate value, NPV. If there are social concerns, private concerns/desires of top management, then there’s a lot of ways the decisions could go.

What’s sad, though, is some of these disruptive shots have profound positive externalities, and a firm that is only considering private profit (NPV), may not take them. Shows the profound positives of a large government role in basic R&D, and even some start-up activity.

I appreciate your post. It seems to me that Apple has been disrupting ‘disruption’. Apple’s model goes to your point exactly. They iterate product design and go-to-market strategies internally and secretly over years, if necessary. //They are committed to testing and retesting their disruption in house so when they succeed, they have bankable revenue and profits locked up and in their sights.//

They don’t do innovation and toss it on the wall.

The big reveal happens only after the device/software/service has been married to a powerful go-to-market strategy. The power of the complete enterprise is applied and -bam- that is launched with speed, surprise, massive marketing and massive supply chain support.

This is how Apple handles this issue: “They will see all manner of potentially disruptive technologies being deployed and instead of removing them from their radar as irrelevant, they should continue to monitor them to see what happens. ”

Apple does all of this internally and secretly over a many year development cycle. Remember Jobs’ famous dictum: He was most proud of Apple’s skill and commitment in powerfully saying “No” thousands of times to arrive at a ‘killer’ bold new product.

They do it over and over again and the best of their competition are copying/stealing this in-plain-sight disruption model as fast as they can.

I think you make very interesting and some valid points about Christensen’s Theory, but I wonder if your observations also miss important subtleties associated with the theory. First of all, your “disruptive model” only covers one of the two models of disruption. The entrant entering into the lower end of the market and riding to the top is the better known disruption model than the lesser but potentially even more important model, in which the entrant builds itself as a viable product in a different market and transports itself into the new market where the incumbent gets disrupted (disruption from adjacency). This model is more difficult to understand for those less familiar with the theory, and it is also more difficult to identify. I-phone is one of these examples where it perfected its customer acceptance in a “phone” market and quickly gained share of the “computing” market. Based on this second model, your two criteria of identifying disruption do not apply well, as in an adjacent market disruption, entrant does not have to exhibit inferior technology (all it needs to do is be used in something different – or different “job” environment), and disruption can’t be noticed easily, as adoption can happen quite rapidly, if the environment evolves to allow the entrant to jump from one (e.g. phone market) to another (e.g. computing market). Your hypothesis on acquisition as a way for incumbent sustaining itself against disruption is a valid option, and this “liquidation” event, being a “discontinuous event” is not exactly accounted for by the theory. However, the M&A model is not a good option when disruptive entrants are many, and the incumbent need to choose only a few of the players (anti-trust issues), or if the incumbent already has an in-house technology that is already disruptive. A good example of this is Kodak, having been the first firm to introduce digital camera, but its digital camera division was unable to grow to be competitive. They certainly did not feel they needed to buy somebody to stay alive, and even if they had bought someone, they would’ve failed to grow it, as incumbent film segment with 85-90% margins would’ve snuffed it out. The publishing industry fell into the same problem. Your paper with Matt Marx in speech recognition industry is a special case, in my view, as the technology of speech recognition is more concentrated (unlike digital camera) that it would’ve been much easier for the incumbents to identify the proper targets. Finally, the disruptive theory DOES NOT suggest that a firm looks for a new product that will cannibalize the incumbent! What it suggests is that the way incumbent firms use discount cash flow model to justify its long-term sustainability is flawed, leading to the very conclusion you provide – “you still lose your entire value of existing business.” By definition, if the incumbent market were to be fully disrupted, your current firm value will approach zero over time, essentially saying that today’s entire value of the firm cannot be preserved. And in some industries like publishing/print media and camera/film industry, the end story was already written the day the digital camera and Kindle were commercialized. So, in order to really appreciate the subtleties of the theory, one must throw away the traditional economic and finance theories, as those theories do not have the ability to account for the “table” (market) turning upside down on all the players involved. And this is why good, rational companies fail, because rational models based on existing assumptions just do not give you the right answers.

Thanks for this column, really appreciated it as I’m reading up more on the Christensen work and critiques.